The increasing rate of large weather and climate disasters are dramatically impacting the commercial real estate business in ways that may not be readily apparent to many.

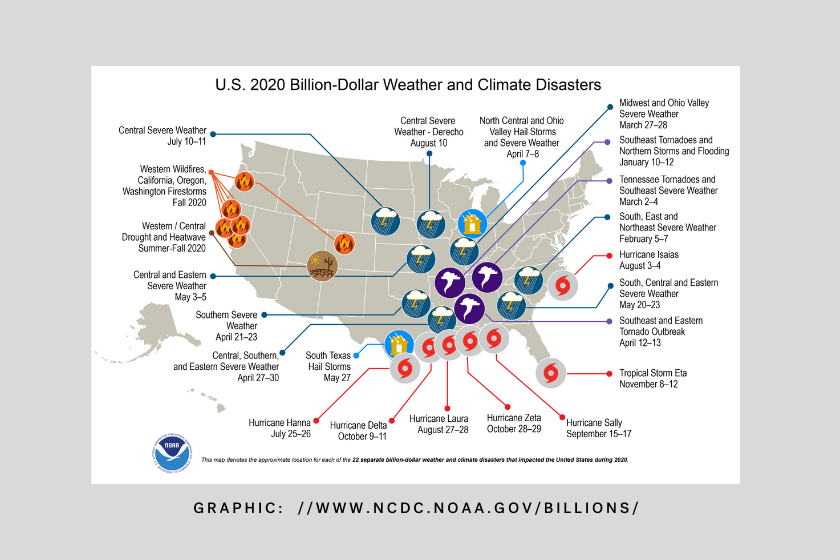

While the headlines in 2020 were filled with political debates and COVID-19 updates, the United States suffered a record number of climate and weather events costing more than $96.4 billion. In addition to these monetary costs, the 22 events, shown in the first image below, were the direct cause of 262 deaths (source: National Centers for Environmental Information). The previous record was 16 events which occurred in 2017 at a cost of $325 billion.

These are not isolated incidents or statistical anomalies. In the past five years, we have averaged 16.2 events per year, up from the 40-year average (1980 – 2020) of just 7.1 per year. Every state in the union has experienced at least one $1 billion disaster in the past 40 years, but Texas has endured the most: 124 $1 billion disasters since 1980.

At the end of 2020, PEG was forced to deal with these rising costs as we searched for property and casualty insurance for our acquisition in Kissimmee, FL. Based on industry standards, we had underwritten insurance costs at $250/unit. After an extensive search throughout the market, we found that many insurers had just pulled out of the Florida market entirely due to steady losses from weather and climate events. When we finally sourced coverage from four different carriers, it ended up costing us $500/unit to cover our conventional risks.

HARD MARKETS

The steep increase in insurance costs was the result of the Florida property insurance market going “hard.” A hard market is one where there is little competition driving prices downward.

Unfortunately, “in the property and casualty insurance industry, price, terms and conditions as well as the availability of coverage and capacity are all impacted by fluctuations between soft and hard markets. As of Q3 2020, [this] insurance market had been considered soft for nearly 15 years but is now trending towards a hard market,” reported Bart Kresse of M&T Insurance Agency on January 25, 2021 in The Business Journals.

Put simply, the insurance market works on basic economic principles and the insurance providers go where they can make money. Based on the recent losses in the “habitational market” of insuring apartments and hospitality properties, many insurers are pulling out of this sector and seeking new business elsewhere, for instance with Cyber Liability. As the inevitable result of these changes, buyers of insurance in catastrophe-prone coastal areas may find capacity constraints where coverage is more and more complicated with excess layers of insurers.

INCREASED COSTS

For 2021, the insurance industry estimates that premiums will increase by an average of 15%. Risk Placement Services (RPS), an industry resource, reports that Hurricane Laura, which hit the Gulf Coast last August, is coming in with total damages at $11-$15 billion. Looking at Utah alone, Willis Tower Watson reports that “non-challenged” properties will see 2021 rate increases of 15-25% and umbrella policies will see increases of 30% to 150% in 2021 (source: https://www.propertycasualty360.com/2021/01/07/hard-market-conditions-expected-in-2021-414-194297/).

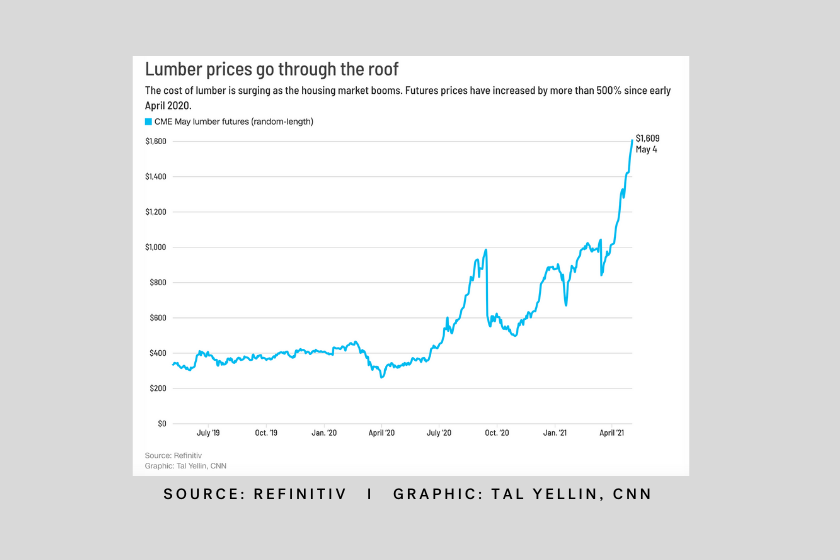

This cost increase is exacerbated by the rising costs of rebuilding. Lumber prices increased more than 500% from April 2020 to May 2021 (see the second image below) and concrete demand is outpacing supply, resulting in increased pricing and slowdowns. According to the National Association of Home Builders, surging lumber prices alone have pushed the average price of a new single-family home $35,872 higher.

If you didn’t budget for the magnitude of these increases in 2021, be sure to incorporate them into your 2022 budgets with similar increases. National Oceanic and Atmospheric Association predicts that due to rising temperatures of the oceans, the 2021 hurricane season has a 60% chance of above-normal hurricane activity (source: https://www.ucsusa.org/resources/hurricanes-and-climate-change#:~:text=The%20rising%20of%20warm%2C%20moist,content%20to%20rise%20as%20well).

RECOMMENDATIONS

Below are some simple tips for handling escalating insurance costs:

- Preventative management of the risks

- Invest in newest technology for monitoring kitchen fire risk

- Selectively screen tenants

- Use video surveillance cameras

- Manage the way your hotel is used for group gatherings

- If you do experience a loss, manage the process closely and with great attention to detail. Use your insurance agent as your advocate.

A POSSIBLE SILVER LINING

Despite the perhaps dire picture reflected in the above data, PEG anticipates that multifamily properties should be buoyed by large increases in rents which may cover the additional insurance costs.